Instead, I'm told, the California disaster was all the fault of Ed McMahon for defaulting on his Beverly Hills mansion.

Of course, the biggest single problem was likely that loosening credit standards to add 5.5 million more minority homeowners (as President Bush demanded in 2002) loosened credit standards not just for minorities but for everybody. But the minority contribution alone was significant. And it's crucial to understand this because it's only going to get more significant as the population of Hispanics increases by about 100 million from 2000 to 2050 (according to Pew Hispanic Center projections).

There are now 100 million minority individuals in the U.S., and while they may or may not have much money, they certainly took out a lot of dubious mortgages in the housing bubble, expecially in California and a few similar states.

One off the things I've been trying to explain is that the late mortgage bubble was so crazy because, unlike most bubbles, it was not a bet on the rich getting richer (as in the Internet Bubble). Betting on smart young people to invent new Internet stuff wasn't nuts -- they actually did invent a whole lot. The nutty part was that there weren't many ways to use an open system to achieve a quasi-monopoly and earn above normal returns on investment.profit from the inventions.

But the housing bubble was a bet on the increasing ability to pay of the part of American society -- the working class and lower to middle-middle class, primarily -- that has been getting the fuzzy end of the lollipop since about 1973.

It was a bet on the bottom 3/4th or so of American society, in particular on the second quartile from the bottom, because that's where the incremental homeowners needed to push the home ownership from 64% to 69% would primarily come from. I'm a strong advocate of the well-being of the bottom 3/4ths of America, but that doesn't mean I ever saw much evidence that they were substantially increasing their ability to pay back massive mortgages. It was all just nuts.

The Dr. Housing Bubble blog has been making this point for a long time about California real estate. For example:

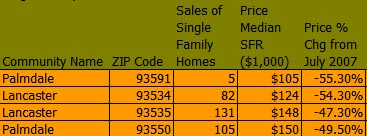

Lowest priced homes in Los Angeles County in July 2008:

Palmdale and Lancaster are in the high desert about 60-75 miles north of downtown LA. Home prices were cut in half there from 2007 to 2008.

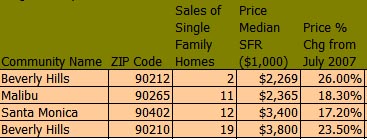

Let us now take a look at these top 4 zip codes in median home price in LA County, where prices were still rising as of July 2008:

Also, note that the most expensive zip codes aren't turning over as fast as the least expensive, so mortgages originated during the carcinogenic years of the bubble don't make up as large a proportion in the high end zip codes as they do in the low end zip codes. There were a lot of people furiously flipping houses in Lancaster to put them on the road to one day moving up to Beverly Hills. But the folks in Beverly Hills already were living in Beverly Hills, so the urge to speculate wildly on their houses wasn't as pressing for them.

Buying a house in Beverly Hills for millions of dollars is a bet that there will always be stars and other rich people with lots of money who'd like to live in Beverly Hills with the other celebrities. That proved to be a fairly good bet during the Great Depression, and a great bet ever since. Buying a home in Lancaster-Palmdale for hundreds of thousands of dollars, however, was a bet that people who work in big box retail store will somehow make dramatically more money in the next decade or two.

Personally, like most red-blooded Americans, I'd love to Blame It on Beverly Hills, but that's not what the evidence says. (Of course, rich people speculated in investment properties, which had disastrous effects on some neighborhoods when they rented out nice houses to lowlifes to bring in a little cash flow while they were waiting to cash in.)

To bring it home, to help you get a palpable feel for what the financial assets that the U.S. Senate wants to use $700 billion of your money to buy, let's look at Dr. Housing Bubble's continuing series on California's Real Homes of Genius, modeled on the old Bud Light commercials:

ANNOUNCER: Bud Light presents real men of genius. Real men of genius. Today, we salute you, Mr. Giant Taco Salad Inventor.

UNIDENTIFIED MALE: Mr. Giant Taco Salad Inventor.

ANNOUNCER: Ground beef, refried beans, guacamole, cheese, sour cream, and if there's any room left, a few shreds of lettuce. A culinary creation that baffles the human mind. A 12,000-calorie salad. Ay carramba. Some may ask, is your taco salad healthy? Of course it is, it's a salad, isn't it? [If you're still hungry] you can eat that deep fried crunchy bowl.

There are 88 different cities in LA County, which is home to over 3% of the country's residents, and nobody can be expected to know, say, Bellflower from Bell Gardens. So, I'll stick to Real Homes of Genius from one low-end municipality that you might have heard of, Compton, home of the Crips gang. This is where the original West Coast gangsta rappers, NWA, were straight outta. Although world-famous as a black ghetto, already by the time of the 2000 Census, it was 56% Hispanic and no doubt was increasingly Latino all through the Housing Bubble.

(When you're looking at these prices below, add a one or two or three hundred thousand to get prices for comparable homes in cruddy nearby neighborhoods that didn't have a nationally notorious brand name.)

Here, for example, is an 828 square foot manse on a 5,000 square foot Compton lot, with one bathroom, built in 1954.

With the inherent value of this kind of asset, is it any surprise that this 828 square foot Compton home's selling price went up, up, up:

On 11/05/2003, it sold for $110,000.

On 9/30/2004, it sold for $235,000.

On 12/22/2005, it sold for $310,000.

But that's nothing. Here's a 500 sq. ft. one bedroom

- one bath Compton house built in 1939.

- one bath Compton house built in 1939.It sold on 9/27/2007 for $340,000.

Think about that. That's $680 per square foot of 68-year-old wood frame construction. In Compton.

By August 2008, less than a year later, it was on sale for $97,900, a 71% price cut in less than a year.

If 500 square feet isn't quite enough to fulfill your lifestyle needs, there is always this 1,089

square foot Compton home. Dr. Housing Bubble explains:

square foot Compton home. Dr. Housing Bubble explains:This 1,089 square foot home includes four bedrooms and two “full” baths. Nestled in the majestic resort town of Compton, you will entertain your friends and family behind U.S. Steel reinforced gates, such as those guarding the Rockefeller Estate. This home uses transcendent features of the 1950s including a patented aqua green color to ward off nuclear attacks from Soviet warships. This moderately priced dream crib is all yours for the rock bottom price of $375,999. This is actually less than the sale price of 2006:What happened to all the money that people in Compton made selling these Real Homes of Genius to each other? A few wise oldtimers presumably bailed out and retired to the South with the profits from selling their Compton homes to Hispanic newcomers. A few clever youngsters probably sold out at the peak and rented homes for $900 per month. A lot of the money, of course, went into buying new Real Homes of Genius. But, I suspect the worst problem is that a lot of people wound up spending the money on consumer goods. In fact, plenty of people probably spent money they assumed they'd make eventually off selling their homes to support a lifestyle that can't be supported. And that's going to require a nasty contraction of the real economy to work out.

Sale History

06/23/2006: $412,000

10/01/1981: $58,500

Beyond that, the global financial markets concocted vast leveraged contraptions on top of these absurdly leveraged no money down Compton mortgages.

My published articles are archived at iSteve.com -- Steve Sailer

26 comments:

While I agree that the housing crash was mostly due to lax lending standards toward minorities (Hispanics and Blacks) in Western states and Florida, along with a few other states, here in North Carolina the main problem which caused the housing crash was/is OVERBUILDING because there aren't all that many Hispanics here (yet) and many Blacks simply don't live in these new subdivisions which are the most affected by the housing crash.

The main reason for the crash was that market here is absolutely flooded with homes in subdivisions all over the place and no one is buying them. There is a vast oversupply here and, I suspect, in many other states in America. It's a basic supply vs. demand issue, really.

Of course this is another reason for the federal government to fling the immigration doors wide open -- they will say it's "because we have a huge oversupply of homes and America's economy will not correct until many of these homes are filled!" Thus, they want to fill them with immigrants.

A solution? White people need to start having more babies to fill all of these homes instead of letting immigrants come in and fill the void.

Beyond that, the global financial markets concocted vast leveraged contraptions on top of these absurdly leveraged no money down Compton mortgages.

Glad you found room to squeeze this in.

This particular aspect involves a minority with a certain je ne sais quoi. An honest observer would have to admit they just might have as much to do with the bubble/bailout as "NAMs".

The good news about North Carolina may be that the ability to build kept the prices down. So, NC with 3.0% of the population had only 1.5% of the foreclosures as of August. That's not great -- it's 20th in the country out of 50 states, but it's not a disaster (at least not yet).

It's paradoxical, though. In places where the regulation climate makes it easier to build, you get more physical waste in a bubble due to unneeded home being constructed. But the financial ramifications aren't as bad as in a restricted building environment like California, where the artificially boosted demand gets converted into higher prices which get turned into bigger mortgages which get turned into more frequent and bigger defaults.

If whites are 90% of the population in a city with 10 school district, then at least 9 school districts are going to be "good school districts." But let's say whites are 50%. If whites are somewhat spread throughout the city--some young and old people living in minority majority areas--then there is going to be a musical chairs rush to get in to the Good School Districts, which may now be only 3 out of the 10 districts.

My prediction is that after moving from the east to the midwest, and then to California, and then to Colorado, alot of whites are going to start moving back to the midwest, especially if the dollar stays weak. Cleveland's housing prices are actually going up.

I gather from reading Steve that there was a definite govt policy to increase housebuying by "visible minorities". Maybe this was because being visible they act as tracers for unfairness that affects all poor(ish) people. In what you seem to regard as the normal and desirable situation with mortgages only granted to the better-off AND a modest but continuous increase in the real value of houses every year, homeowners are getting something for nothing. I think it was one of Kingsley Amis's novels that pointed out that this means someone else is getting nothing for something. In this case the losers are renters. If VMs are disproportionately renters, this becomes visible.

I think there's a good chance that the high end housing collapse will be almost as bad as the low end collapse, but it just hasn't yet hit.

Many of the people living in those $10M and $20M mansions think they're still rich and can afford them.

But they put much of their own money into hedge funds, and the hedge funds put that money into mortgage securities, and the mortgage industry put it into those low end homes. Most of the hedge fund money is gone, but not being subject to public reporting like Goldman or Lehman, many of their clients aren't yet aware of this.

Once reality sets in, lots of those $15M Beverly Hills mansions will start going on the market for $10M...then 7M...then $4.5M. And the cycle will continue.

The only bottom will come if wealthy non-dollar foreigners swoop in to buy up B.H. housing with cheap dollars, and I'm not sure at what level that will occur.

With the economy contracting, it is not clear that 100M illegals will want to come to the US.

NC-er: Of course this is another reason for the federal government to fling the immigration doors wide open -- they will say it's "because we have a huge oversupply of homes and America's economy will not correct until many of these homes are filled!" Thus, they want to fill them with immigrants.

A solution? White people need to start having more babies to fill all of these homes instead of letting immigrants come in and fill the void.

True, American Caucasians & Asians need to start making more babies:

USA Caucasian Population By Age

USA Asian Population By Age

However, if we could use this crisis to import 20 million [or more] young, fertile Europeans wishing to flee the imposition of Dar al Islam in Eurabia, and another 20 million [or more] young, fertile Chinese Christians wishing to flee the Chicoms' 1-child policy, then I say: OPEN THE FLOODGATES.

Getting white people to have more babies is probably impossible whatever happens. But if this were to work at all you'll have to get them to marry and stay married. Since divorce requires two houses where instead of one that might help the housing glut, but do nothing long term to reverse these economic and social trends. More single women are using sperm donors, but if that is the best we can do I don't think it's worth it.

they will say it's "because we have a huge oversupply of homes and America's economy will not correct until many of these homes are filled!" Thus, they want to fill them with immigrants.

I've already predicted that, and the bailout just passed does indeed give the government power to buy "distressed assets," and I would wager big money that we will soon be hearing that we must have higher immigration levels and amnesty 'or else the government will get stuck with all these homes.'

You will be hearing that refrain from a major amnesty playa - McCain, Obama, the Wall Street Journal, the Chamber of Commerce - within a year.

However you're statement vis-a-vis Hispanics in North Carolina is at least partly wrong. North Carolina saw a 394% increase in its Hispanic population in a single decade (76,000 to 378,000), and the Hispanic population there is probably now over half a million. And while Hispanics in NC were probably never doing much of the buying, I'd wager they were doing a ton of the building.

Which is a key point: the mortgage meltdown is not just about minorities defaulting on easy loans. An Ohio State study recently showed that much of the trouble is due to real estate speculators and commercial construction.

The flood of cheap illegal labor contributed to this crisis by allowing supply to vastly outpace demand, whether in first homes, investment homes, or commercial properties. There is thus a more direct link to immigration (and specifically illegal immigration) than "Hispanics defaulted on loans."

Builders were overbuilding because they had the labor and money to do it with. Banks supplied the money. Illegal immigration supplied the labor. Americans are now supplying the money to bail them out. Cheap homes, my ass.

However, if we could use this crisis to import 20 million [or more] young, fertile Europeans wishing to flee the imposition of Dar al Islam in Eurabia...then I say: OPEN THE FLOODGATES.

And turn Europe over to the Muslims? I like Europeans, but Europeans need to start breeding there and white Americans need to start breeding here.

There is no reason (yet) to retreat and consolidate our numbers. We still hold the high ground. Sanity can yet prevail.

"What happened to all the money that people in Compton made selling these Real Homes of Genius to each other? A few wise oldtimers presumably bailed out and retired to the South with the profits from selling their Compton homes to Hispanic newcomers. A few clever youngsters probably sold out at the peak and rented homes for $900 per month.

Actually, the pre-bubble owners were probably bought out by a local with a Realtors license, who then recruited a local underground economy member, or new/illegal immigrant, or sorta homeless guy, to 'buy' the place with all the 'qualification' and other loan paperwork done by the Real Estate guy, ie the seller, and the 'appraisal' done by his buddy/brother, and the mortgage provided another buddy/family member.

I'm a white person having babies, and I just moved out of North Carolina, in part because of the completely insane overdevelopment. Did you not notice the MASSIVE DROUGHT in the summer of 2007? Did you not notice the total failure of local government to handle it? Whee, let's destroy woodlands and wetlands to build ugly crap houses when we not only don't have enough roads or schools, we don't have enough WATER. AWESOME.

And it goes without saying, ALL those nasty ugly developments are completely automobile dependent. The way things are planned out there, you literally cannot walk to where you'd like to go even if you're willing to. No sidewalks, no bike trails, just PF Changs parking lots and giant highways. What a bunch of evil morons. Who the hell would want to live in that clusterfuck? Oh wait, I know - people moving here from third world hellholes! It's better than a refugee camp!

Perhaps the bailout is not really designed to protect mortgage holder who can't pay for their mortgages, but is really designed to protect those highly leveraged individuals who would be heavily in debt if the value of those mortgages is wiped out.

If you care to learn something on the cause of this crisis, versus using it to promote some crusade, I suggest you look at Austrian economics.

Austrian writings on business cycles and credit booms are easy enough to understand, and you'll find they predict what we have witnessed quite well.

You'll earn that blaming various market players is sadly misplaced. Their whole purpose should be to get rich in any legal way they can. It's misguided easy money policies that got us in this mess.

But don't let the truth stop you from your futile crusade to diss on the less fortunate.

Did you not notice the total failure of local government to handle it? Whee, let's destroy woodlands and wetlands to build ugly crap houses when we not only don't have enough roads or schools, we don't have enough WATER. AWESOME.

The Catawba River is listed as the most endangered waterway in the US thanks to the urban sprawl of Charlotte. All because of those damned immigrants! (I'm talking about Yankees, of course).

But don't let the truth stop you from your futile crusade to diss on the less fortunate.

Who are "the less fortunate"? Certainly not the "NAMs" who have been the focus of the discussion on this blog. They got and will continue to get preferential treatment.

Likewise the wealthy minority that's disproportionately involved in the anti-racism, oversight, and financing portions of this unprecedented transfer of wealth. They've enriched themselves.

The "Austrians" and their materialist cousins the Marxists both advise us to cover our lying eyes and say: minorities, what minorities, all we see is money.

Setting this selective and mendacious blindness aside, the truth is that several minorities, "visible" and not, have disproportionately participated and benefited from either the bubble, the bullshit ("leveraged contraptions"), or the bailout. Meanwhile, "middle class" "Main Street" disproportionately White Americans have been disproportionately harmed.

Looking beyond short-term financial considerations Whites are also being rapidly transformed into a minority by the very mass immigration upon which the circular bubble logic is based. The cost to us is incalculable.

Of course the managerial class will foist more of the same upon us. It gives their plutocrat bosses precisely what they want: perpetuation of an increasingly pluralistic pyramid scheme. By the time the pyramid collapses the various low-level minorities, including Whites, will be that much more easily managed into blaming each other rather than the minority on top.

If you care to learn something on the cause of this crisis, versus using it to promote some crusade, I suggest you look at Austrian economics.

And if you care to learn about the shortcomings in the Austrian school, I suggest you look at Caplan's Why I Am Not an Austrian Economist:

"Mises and Rothbard certainly produced an original alternate paradigm for economics--and applied this paradigm to a number of interesting topics. Unfortunately, the foundations of their new paradigm are unfounded, and their most important applied conclusions unsound or overstated."

1/ Look on the bright side (is that legal these days?):

A huge housing price crash makes 'affordable family formation' more of a reality.

2/ And there are groups of Whites who are having lots of babies-but no one here likes them.

(Still no attempts to bring in Georgians to Georgia)

"Anonymous said...

And it goes without saying, ALL those nasty ugly developments are completely automobile dependent. The way things are planned out there, you literally cannot walk to where you'd like to go even if you're willing to. No sidewalks, no bike trails, just PF Changs parking lots and giant highways. What a bunch of evil morons. Who the hell would want to live in that clusterfuck?"

Someone's been reading James Kunstler.

"Anonymous said...

If you care to learn something on the cause of this crisis, versus using it to promote some crusade, I suggest you look at Austrian economics.

Austrian writings on business cycles and credit booms are easy enough to understand, and you'll find they predict what we have witnessed quite well.

You'll earn that blaming various market players is sadly misplaced. Their whole purpose should be to get rich in any legal way they can. It's misguided easy money policies that got us in this mess."

I'll blame whomever I damn well want, jerkoff. I do not believe that to "get rich in any legal way" is a worthy or honorable occupation. Some ways are better than others. Some ways are not good at all.

Producing mexican midget/donkey porn may be legal for all I know. Is that how you want to maximize your growth function?

It is that kind of amoral, econometric thinking - which worships money and only money - which is bringing this country low.

Someone's been reading James Kunstler.

I hate Kunstler with a fiery passion. He's a corny preacher with no faith but faith in the apocalypse. And while he's a religious zealot who is more interesting in bringing hellfire down on the infidel than he is in making America better, he's right about AWFUL, AWFUL car-dependent development. He just really LIKES it because it gives him more sinners to sneer at.

He doesn't own the word "clusterfuck." It IS a clusterfuck out there.

It's misguided easy money policies that got us in this mess.

But don't let the truth stop you from your futile crusade to diss on the less fortunate.

See http://online.wsj.com/article/SB122298982558700341.html

Russ Roberts cites the CRA, etc., so obviously Austrians don't believe it was purely an easy credit issue.

Lots of blame to go around. Don't stick your head in the sand on the issues here that cause you discomfort.

Check out Barney Frank's huge conflict-of-interest re. Fannie Mae:

Lawmaker Accused of Fannie Mae Conflict of Interest

"Unqualified home buyers were not the only ones who benefitted from Massachusetts Rep. Barney Frank’s efforts to deregulate Fannie Mae throughout the 1990s.

"So did Frank’s partner, a Fannie Mae executive at the forefront of the agency’s push to relax lending restrictions...."

And if you care to learn about the shortcomings in the Austrian school, I suggest you look at Caplan's Why I Am Not an Austrian Economist:

And did Caplan warn of this "greatest economic crisis since the great depression." You'll find most followers of the Austrian school have been warning of such a crisis for years. Unlike pretty much every one of the mainstream economists that use dubious econometric theories to everyone's downfall.

"Anonymous said...

"Someone's been reading James Kunstler."

I hate Kunstler with a fiery passion. He's a corny preacher with no faith but faith in the apocalypse."

My apologies if my tone sounded snarky. I merely meant to point out the connection.

I think that Kunstler is on to a few things - the cheap-oil-centric nature of our country, the degraded state of our society, and the god-awful ugliness of modern architecture.

However he's blinded by being a yellow-dog democrat, and by the fact that he's an insufferable prick. He clearly hates blue-collar folks in general and southerners in particular, whom he considers to be a hopeless, unwashed lumpen proletariat - almost a different kind of species from nice liberals like himself.

I also find it funny that he jets all over the country decrying our addiction to oil. But he is, after all, an important man. Too important for example to express any interest in his readers' opinions - he maintains one of the few blogs I've ever seen with no comments section or even an E-mail address to reach him at. He has essentially told his readers - "I'm too important to be bothered by you low-lifes. F**k off!"

If Kunstler could ever be bothered to read Sailer, he might have a better understanding of some of the social trends he decries.

Post a Comment